NEW FUNDING FOR GLOBAL SOVEREIGNS PROMOTES STRATEGIC ASSET ALLOCATION TO EMERGING MARKETS AND ALTERNATIVES –INVESCO STUDY

-

Emerging markets remain winners of new global sovereign assets – despite overall underlying preferences, at a total portfolio level, for developed markets

-

Allocations to alternative investments increasing on a net respondent view basis - including real estate and private equity

-

Increase in new funding encourages global sovereigns to allocate assets strategically rather than tactically

-

Sovereign investor risk appetite and time horizons increasing, while home market bias decreasing

-

UK the most attractive international market to sovereign investors

Conducted amongst more than 50 individual sovereign investors across the globe, representing $5.7 trillion2 of assets, this year's study reveals emerging markets - including Latin America, Africa and China – continue to be the winners of new global sovereign flow, despite a fundamental preference, relative to the total portfolio, for developed markets. Furthermore, sovereign investors continue to favour alternative investments with allocations increasing across all major alterative asset classes, including real estate and private equity, on a net respondent view basis.

Analysis of data within the study highlights that these geographical and asset class shifts can be attributed to the influence of strategic asset allocation over tactical asset allocation3 in influencing investment strategy and driving investment decisions of global sovereign investors. One influencing factor for this is the expectation of new funding. Almost half (46%) of sovereign investors expect to see an increase in new funding in 2014 beyond the levels seen in 2013, with clear implications on global capital flow.

Increasing new allocations to alternative investments

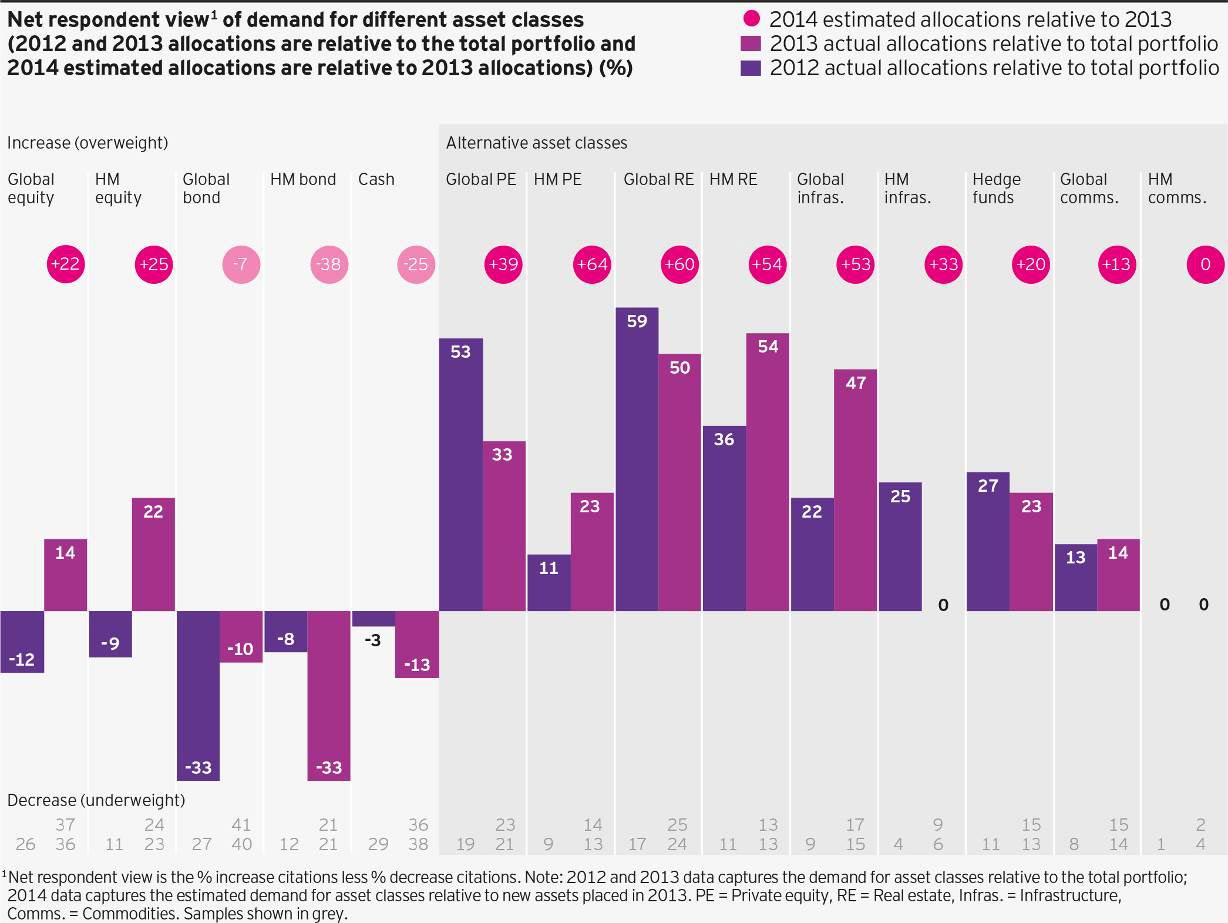

Alternative investments remain the clear asset class winners in terms of new asset allocation within sovereign investor portfolios [figure 1], mirroring the trend reported in the 2013 study. On a net respondent view basis, 51% of sovereign investors increased new exposure to real estate in 2013 and 29% to private equity, relative to the total portfolio. In fact, sovereign investors expect to increase new allocations across all major alternative asset classes in 2014 based on net responses – real estate, private equity, infrastructure, hedge funds and commodities - relative to their 2013 asset placements.

Analysis of the findings suggests this continued appetite for alternatives is a structural trend driven by the influence of allocating assets strategically, rather than a short term shift due to tactical allocations to boost short term returns.

Firstly, many sovereign investors remain underweight in alternatives relative to their strategic asset allocation targets. These sovereign investors had increased their target allocations for alternatives in the last five years and had yet to reach these targets. Secondly, many sovereign investors (46%) expect funding levels to increase in 2014 relative to 2013 [figure 2a]. A large increase in assets encourages more strategic allocation placements since allocating significant assets tactically could lead to breaching internal guidelines.

The third reason that increasing appetite for alternatives should be attributed to strategic rather than tactical asset allocation is the fact that alternatives underperformed during this period, with sovereign investors typically citing an average return of 7% for alternatives in 2013, compared to a target of 8% - which indicates that increasing their overweight in these asset classes is a long-term, strategic decision, rather than a tactical move.

Nick Tolchard, Co-Chair of Invesco's Global Sovereign Group & Head of Invesco Middle East, said: “Given alternatives underperformed during the period in which their allocations increased, it is clear that a strategic asset allocation strategy is driving sovereign investors to alternatives, rather than tactical allocation. The expected net increase in new funding this year is another key factor that explains this preference for alternatives, driven by increasing country surpluses and strong support from governments for their sovereign funds. However, the main reason is that many sovereign investors, especially those with assets in excess of US$50 billion, are seeing it take time to deploy assets in alternatives and emerging markets and are yet to reach the asset allocation targets set five years ago.”

Within alternatives, global infrastructure was particularly popular, with 47% of sovereign investors citing an increase in exposure to new global infrastructure in 2013 relative to their portfolio on a net respondent view basis, compared to 22% in 2012 [figure 1]. Furthermore, sovereign investors expect allocations to increase again in 2014 on a net respondent view basis, with 53% of sovereigns citing an anticipated increase in allocations in 2014 relative to 2013 allocations, as real estate yields continue to fall and global demand, especially for developed market real estate, continues to grow. The risk-adjusted returns offered through investing in global infrastructure also appear to be a key driver.

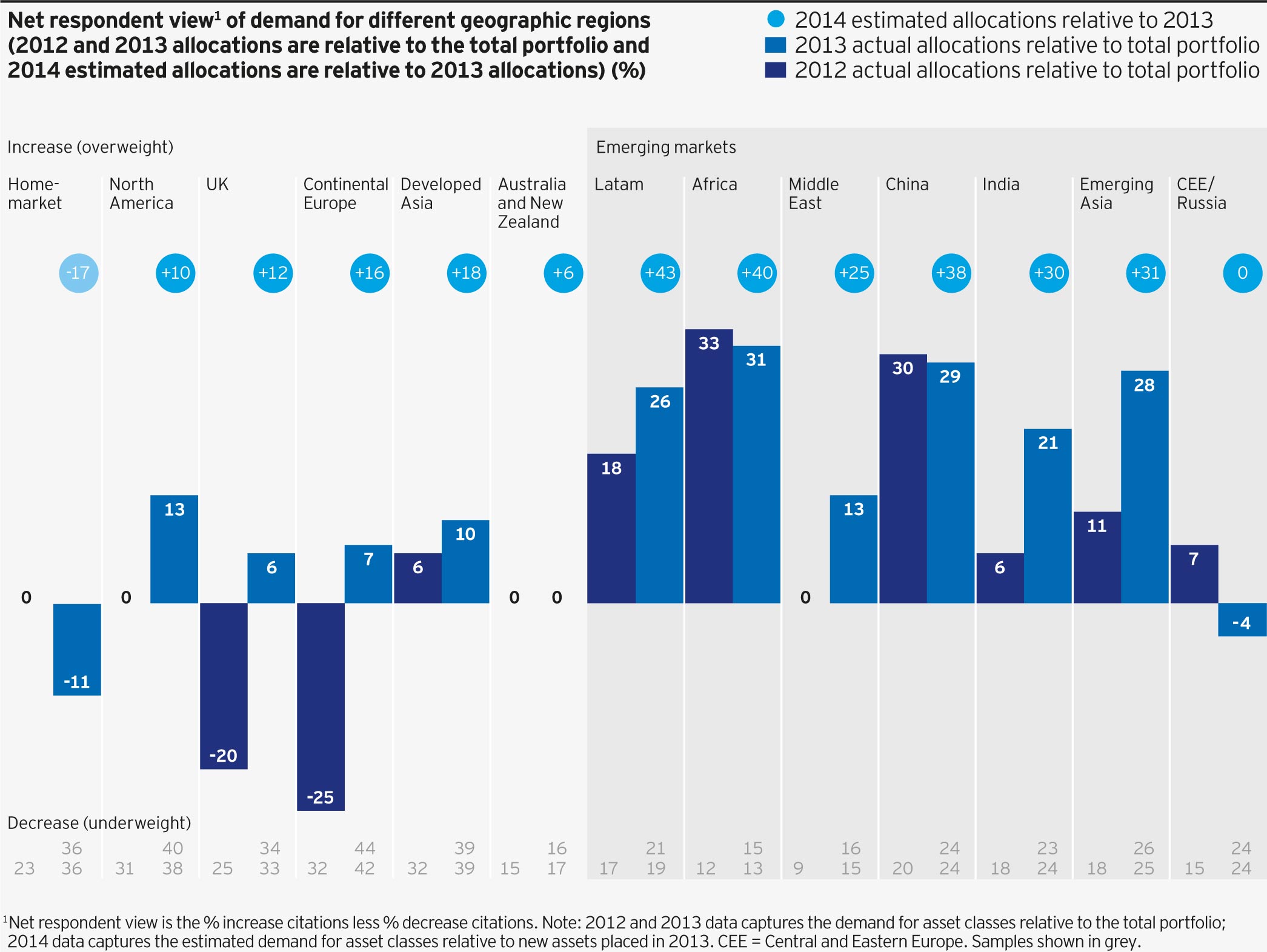

Growth in new capital flow to emerging markets – but fundamental preference for developed markets remains As observed in the 2013 study, the flow of new global sovereign assets continues to reach emerging markets with new allocations to Latin America, Africa, China, India and Emerging Asia all increasing in 2013 based on the net respondent view and relative to the portfolio, and are expected to increase again in 2014 relative to 2013 [figure 3].

Similarly to alternatives, this trend appears to be largely driven by strategic allocation targets. Feedback from sovereign investors indicates they are underweight in emerging markets relative to their strategic asset allocation targets, giving them more room to increase new exposure to the regions. This long term structural trend to emerging markets does not appear to have been influenced by the fact that emerging market equities underperformed developed market equities during 2013.

There are some exceptions where tactical asset allocation strategies are at play, such as Central Eastern Europe and Russia. These are the only emerging markets to which weightings declined on a net respondent view basis in 2013 and to which respondents expect exposure to remain flat going forward into 2014, primarily due to political instability.

However, while the major trend in geographic allocation is a strategic shift to emerging markets, with allocations set to increase from current levels, this takes place within the context of a strong historical preference for developed markets, relative to the total portfolio. Many sovereign investors expect to remain underweight in emerging markets on a GDP weighted basis. Even after excluding home-market allocations from sovereigns based in developed markets, 56% of the average sovereign investor portfolio is in developed markets.

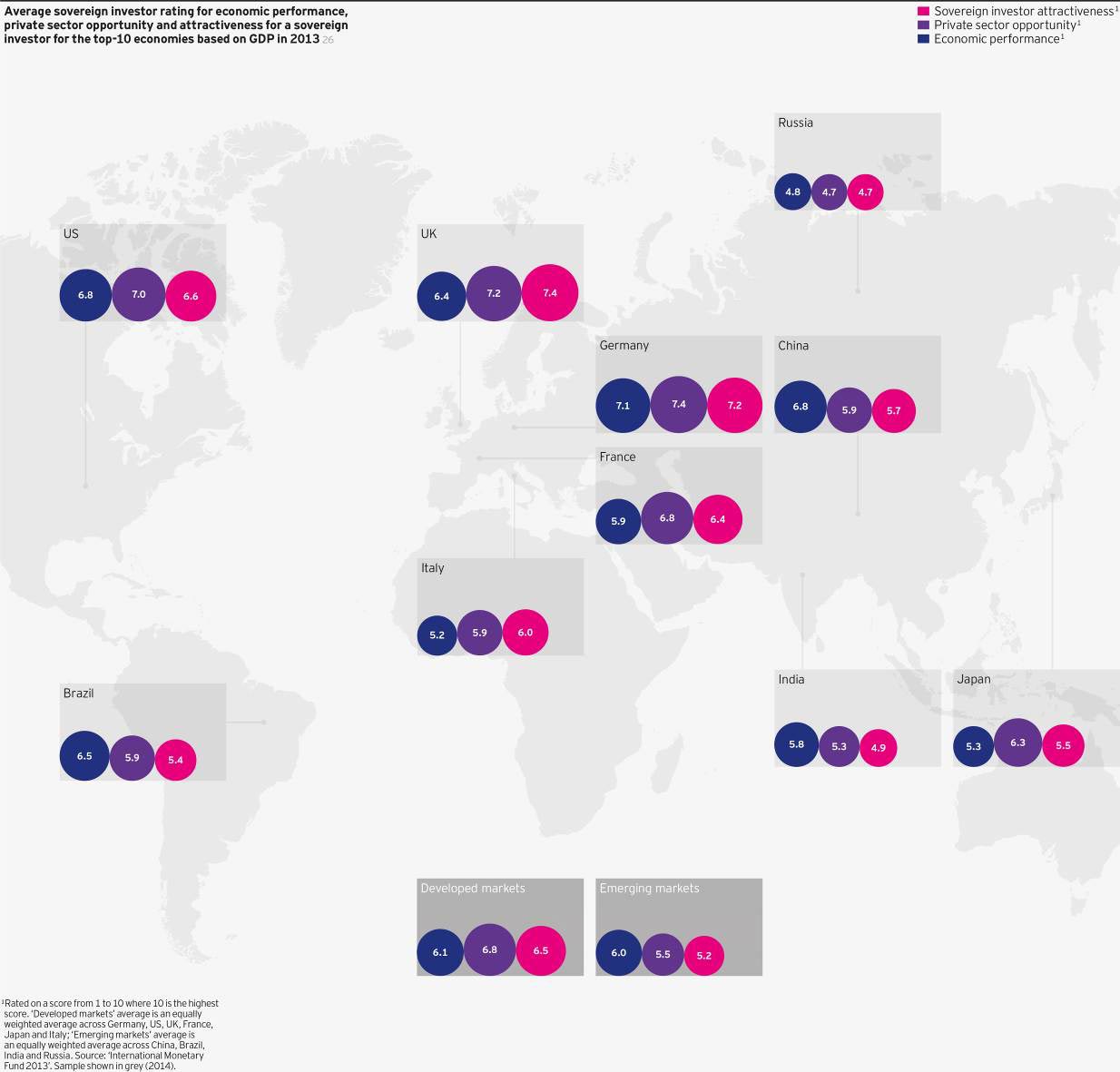

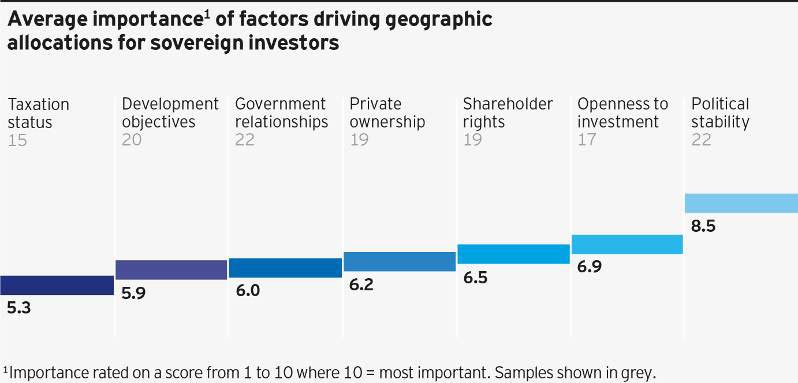

Figure 4 shows average sovereign investor ratings for economic performance, private sector attractiveness and attractiveness for the top-10 economies based on size. In terms of attractiveness to sovereign investors, the perceived average economic performance rating for developed and emerging markets are comparable, however there is significant variation in the overall attractiveness of the economies for sovereign investors, ranging from 4.9 (India), to 7.2 (Germany) and 7.4 (UK). Interestingly, sovereign investor attractiveness scores are lower relative to private sector opportunity in the US, but higher in the UK, which leads the UK to be considered the most attractive international market to sovereign investors globally. Germany's scores are also strong and ranked highest of all markets on economic performance and private sector opportunities, yet its score decreases relatively on sovereign investor attractiveness.

Nick Tolchard commented: “Despite allocations to emerging markets set to increase, a strong underlying preference for developed markets is still apparent, with sovereigns attracted by their depth, stability and diversification benefits, the latter of particular importance to sovereign investors based in emerging or frontier markets. Various factors determine sovereign geographic allocations – most notably political stability, openness of a country to sovereign investment, strength of shareholder rights, level of private ownership, and government relationships. The UK's attractiveness can be attributed to its perceived political and economic stability, openness to foreign investment, and sovereign investors are attracted by the alternative investment opportunities offered in the UK.”

Increasing risk appetite and time horizons, and reducing home market bias

The geographical and asset allocation preferences of global sovereign investors are also indicative of their current risk appetite and time horizons, and bias towards their home market.

In 2012, sovereign investors increasing new asset placements in alternatives typically cited a decrease in equities and global fixed income. Similarly, those increasing new exposure to emerging markets were typically decreasing exposure to developed markets. Yet in 2013, these dynamics changed and those increasing new allocations to alternatives instead decreased their allocation to home-market fixed income or cash, rather than global fixed income or equities. In fact, home market and global equity allocations increased on a net respondent view basis (Figure 1).

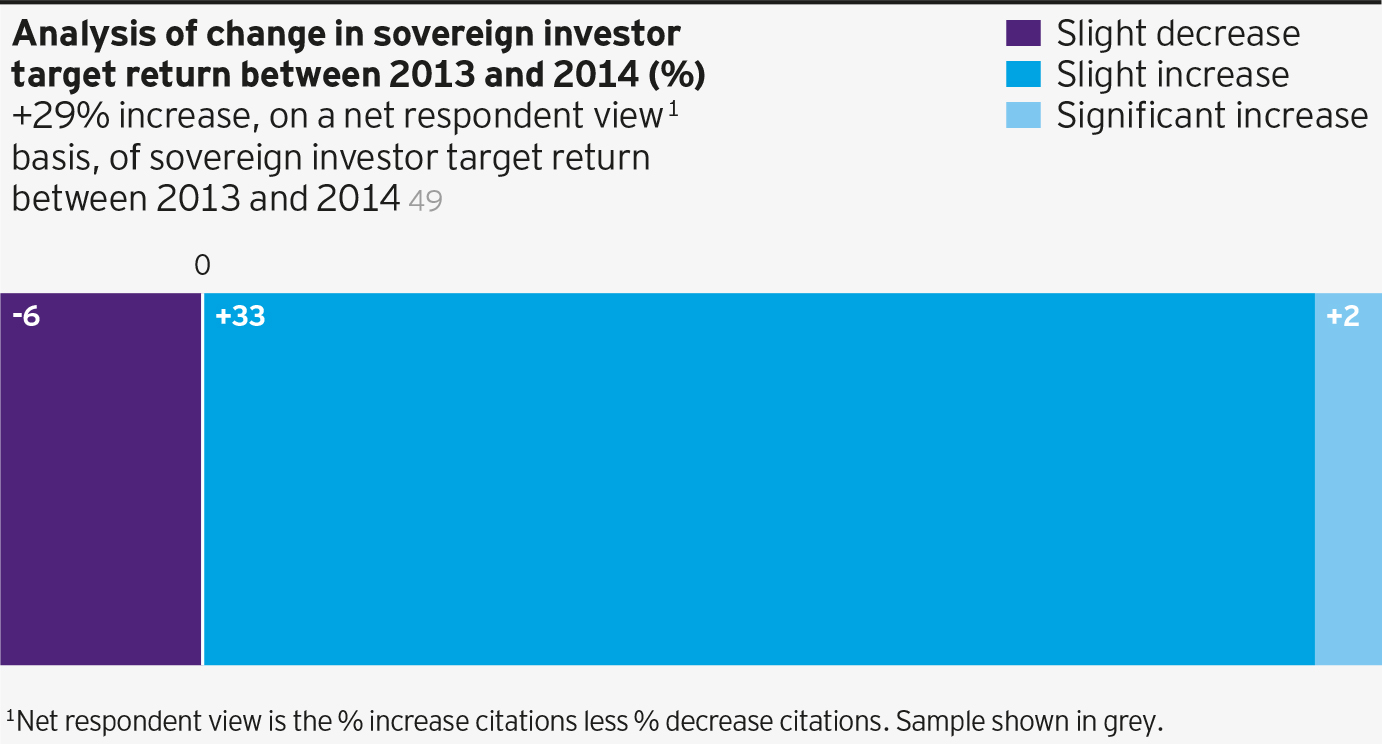

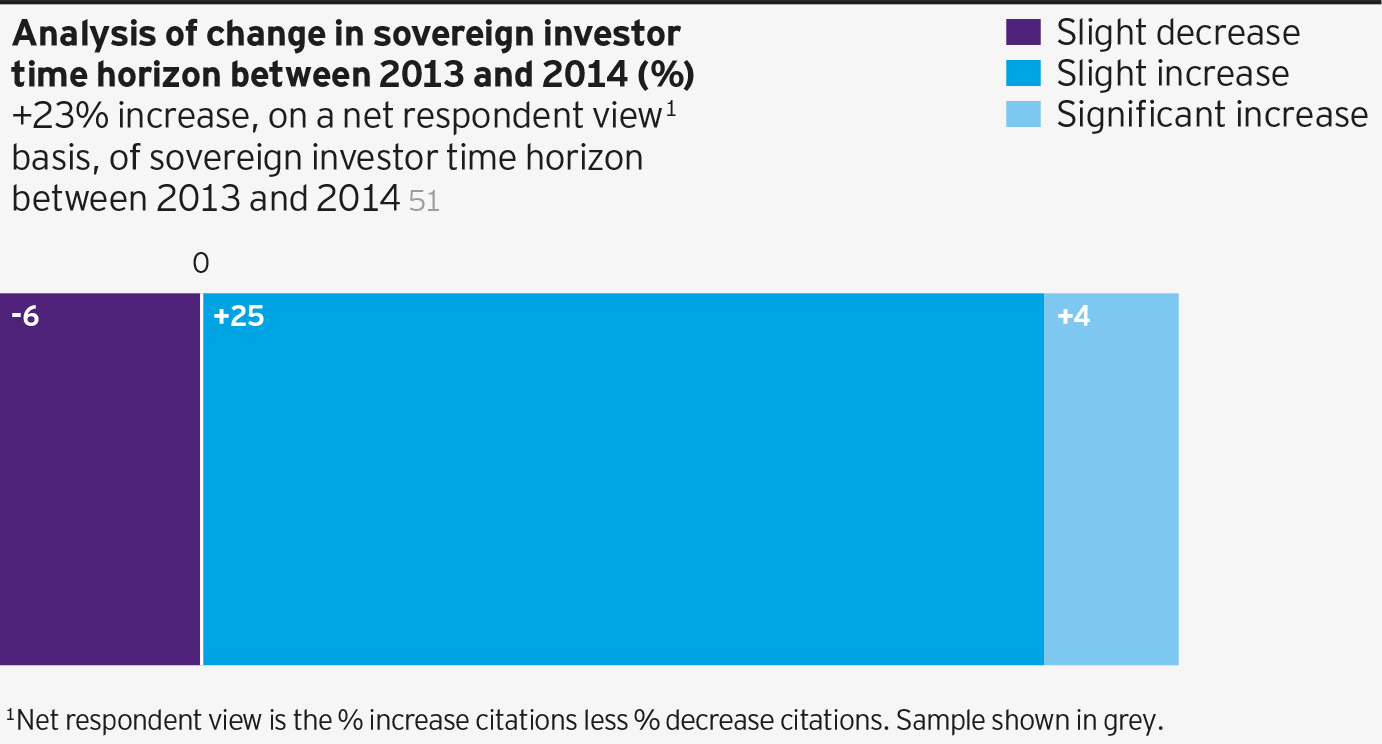

An average increase in target returns and lengthening of time horizons can also be observed in this year's study, which is consistent with increasing exposure to risk assets like equities [figures 6 and 7]. Furthermore, those increasing new assets in emerging markets in 2013 typically cited a decrease in home market allocations rather than developed markets, with 11% of sovereign investors having reduced home market allocations in 2013 on a net respondent view basis [see Figure 3].

Nick Tolchard commented: "Home market allocations usually account for a significant percentage of a sovereign investor portfolio – 42% on average across all sovereign investors in 2013 – so this globalisation is an important change. If allocations to home markets continue to decrease, we could see sovereign investors continue increasing exposure to both emerging markets and developed markets simultaneously. It will be interesting to see how this plays out amongst sovereign investors over the course of this year and how this continues to impact on global capital."

Nick Tolchard concluded: "Sovereign investors are likely to take on a major role in shaping the global economy moving forward so it's essential we remain well informed on their evolving behavioural trends. By commissioning this in-depth study on an annual basis, we're able to develop a much deeper understanding about what drives the flow of sovereign investor capital. This year's findings indicate short-term trends are driven by long-term strategic thinking, and emerging markets and alternatives are becoming firm fixtures in sovereign investors' strategic asset allocations, despite a deep-rooted faith in developed markets that still remains. It's this information that proves invaluable to the industry's understanding of sovereign investors across the globe and to the development of the right solutions to meet their varying needs."

- Ends -

For more information please contact:

Bill Hensel

Invesco

404-479-2886

[email protected]

Notes to Editors:

Figures have been calculated relative to the total portfolio on a 'net respondent view' basis

1. This is Invesco's second sovereign asset management study. In 2014 we conducted interviews with 52 different sovereign investors compared to 38 in 2013 with significant increases in our coverage of liability sovereigns and of Asia and the Middle East regions. Throughout the report we present 2014 results based on the 52 interviews and 2013 results based on 38 interviews. However we have also validated our findings using 'common cohort' analysis of the 31 interviews conducted with the same firms in both years. The breakdown of the 2014 interview sample split by three core segmentation parameters (sovereign investor profile, region and size of FUM) is displayed in figures 26 to 28.

In this study Invesco defines sovereign investors as state-owned investors, which includes: standalone Sovereign Wealth Funds (SWFs), state pension funds, Central Banks and government ministries.

The Invesco Global Sovereign Investor Model bases its segmentation on investment objectives and outlines four key profiles:

Source: Invesco Global Sovereign Asset Management Study 2013

Based on the sample in 2013 study of 37 global sovereign investors

2. Sourced by NMG Consulting: total assets of those sampled stands at $5.7 trillion as at 31 December 2013.

3. Strategic Asset Allocation is defined as investment strategy that involves setting target allocations for various asset classes, while Tactical Asset Allocation is defined as an active portfolio strategy that rebalances asset classes which fall by the wayside.

Charts:

Figure 2a: Sovereign investor view of future funding levels relative to last year's new funding (%)

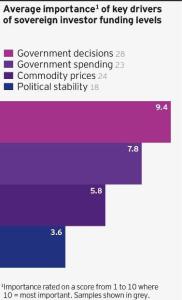

Figure 2b: Average importance1 of key drivers of sovereign investor funding levels

Figure 5: Average importance1 of factors driving geographic allocations for sovereign investors

Figure 6: Analysis of change in sovereign investor target return between 2013 and 2014 (%)

Figure 7: Analysis of change in sovereign investor time horizon between 2013 and 2014 (%)

About Invesco Ltd.:

Invesco Ltd. is a leading independent global investment management firm, dedicated to helping investors worldwide achieve their financial objectives. By delivering the combined power of our distinctive investment management capabilities, Invesco provides a wide range of investment strategies and vehicles to our retail, institutional and high net worth clients around the world. Operating in more than 20 countries, the firm is listed on the New York Stock Exchange under the symbol IVZ. Additional information is available at www.invesco.com.

The Invesco Global Sovereign Asset Management Study is intended only for Qualified Investors in Switzerland and for Professional Clients in other Continental European countries, Dubai, Jersey, Guernsey, Isle of Man and the UK, for Institutional Investors in the United States, Australia and Singapore, for Professional Investors only in Hong Kong, for Persons who are not members of the public (as defined in the Securities Act) in New Zealand, for accredited investors as defined under National Instrument 45–106 in Canada and for one-on-one use with Institutional Investors in Bermuda, Chile, Panama and Peru. This document is for information purposes only and is not an offering. It is not intended for and should not be distributed to, or relied upon by, members of the public. Circulation, disclosure, or dissemination of all or any part of this material to any unauthorised persons is prohibited.

This document is issued in:

Dubai by Invesco Asset Management Limited, PO Box 506599, DIFC Precinct Building No.4, Level 3, The Gate Precinct, Dubai, United Arab Emirates. Regulated by the Dubai Financial Services Authority.

The Isle of Man by Invesco Global Asset Management Limited George's Quay House 43 Townsend Street Dublin 2 Ireland. Regulated in Ireland by the Central Bank of Ireland.

Jersey and Guernsey by Invesco International Limited 2nd Floor Orviss House 17a Queen Street St Helier Jersey JE2 4WD. Regulated by the Jersey Financial Services Commission.

The UK by Invesco Asset Management Limited, Perpetual Park, Perpetual Park Drive, Henley-on-Thames, Oxfordshire RG9 1HH. Authorised and regulated by the Financial Conduct Authority.

The US by Invesco Advisers, Inc. Two Peachtree Pointe, 1555 Peachtree Street, NE, Atlanta, GA 30309

Photo Gallery

-

Net respondent view1 of demand for different asset classes (2012 and 2013 allocations are relative to the total portfolio and 2014 estimated allocations are relative to 2013 allocations) (%) -

Sovereign investor view of future funding levels relative to last year’s new funding (%) -

Average importance1 of key drivers of sovereign investor funding levels -

Net respondent view1 of demand for different geographic regions (2012 and 2013 allocations are relative to the total portfolio and 2014 estimated allocations are relative to 2013 allocations) (%) -

Average sovereign investor rating for economic performance, private sector opportunity and attractiveness for a sovereign investor for the top-10 economies based on GDP in 2013 -

Average importance1 of factors driving geographic allocations for sovereign investors -

Analysis of change in sovereign investor target return between 2013 and 2014 (%) -

Analysis of change in sovereign investor time horizon between 2013 and 2014 (%) -

Sovereign Investors Chart